Government Loan Schemes In 2026: Smart Funding Options Every Indian Must Know [With Calculators]

![Government Loan Schemes In 2026: Smart Funding Options Every Indian Must Know [With Calculators]](https://governmentcsc.com/wp-content/uploads/2026/03/Government-Loan-Schemes-In-2026-Smart-Funding-Options-Every-Indian-Must-Know-With-Calculators.webp)

Government Loan Schemes In 2026: Smart Funding Options Every Indian Must Know [With Calculators]

In 2026, getting access to money is no longer the biggest challenge for Indians. The real challenge is choosing the right government loan scheme that fits your needs. Whether you want to start a small business, grow an existing MSME, fund your education, or secure your family’s future, the government has created multiple schemes that are practical and accessible.

What makes this year different is the upgrades. Many schemes now offer higher loan limits, better subsidies, and faster approvals through digital platforms. You no longer need heavy collateral or complex paperwork in many cases. These schemes are designed to support real people such as small shop owners, street vendors, students, women entrepreneurs, and artisans.

In this blog post we will learn about the most important government loan schemes in 2026, how they work? who should apply? & how to choose the right one based on your goals?

This guide is built to help you take action and not just read information. Along with this you will find interactive tools to find the emi related to each schems. So keep reading…

Table of Contents

Why Government Loan Schemes Are Important In 2026

Access to credit has always been a challenge in India. Many small businesses and individuals struggle to get loans from banks due to strict requirements. Government schemes solve this problem by reducing risk for banks and making loans easier for people.

In 2026, the government has focused more on financial inclusion. This means more people can now get access to funds. Women entrepreneurs, rural businesses, and small vendors are getting strong support.

Another major change is digital transformation. Many schemes now allow online applications. This reduces time and increases transparency. People can track their loan status and get approvals faster.

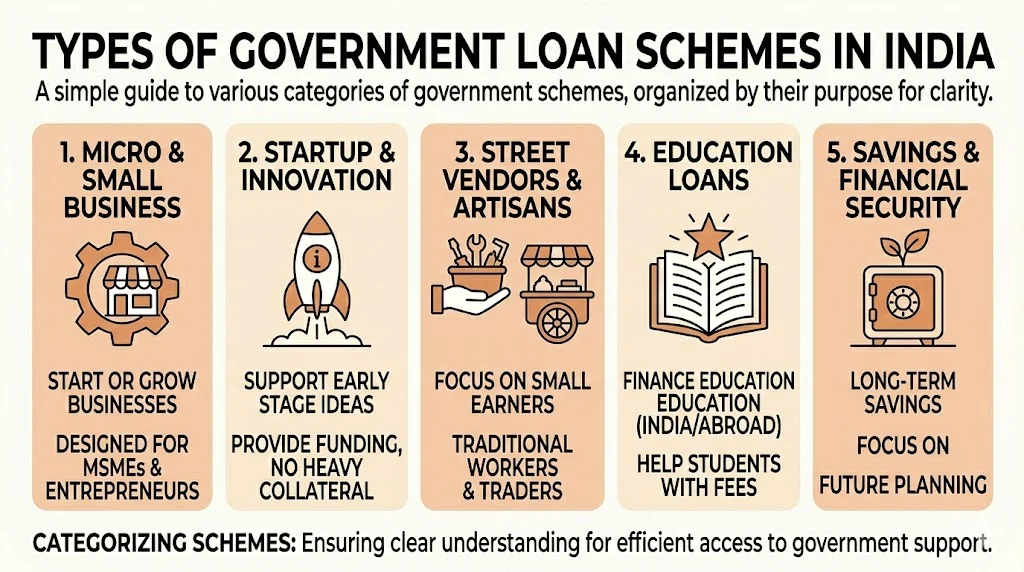

Types Of Government Loan Schemes In India

To make things simple, government schemes can be divided into categories based on their purpose.

- Micro And Small Business Loans: These are designed for small entrepreneurs and MSMEs. They help people start or grow their businesses.

- Startup And Innovation Funding: These schemes support new ideas and early stage startups. They provide funding without heavy collateral.

- Street Vendors And Artisans: These schemes focus on small earners like street vendors and traditional workers.

- Education Loans: These help students finance their education in India or abroad.

- Savings And Financial Security: Some schemes are focused on long term savings and future planning.

Understanding these categories helps you quickly identify which scheme is right for you.

Top Government Loan Schemes You Should Know In 2026

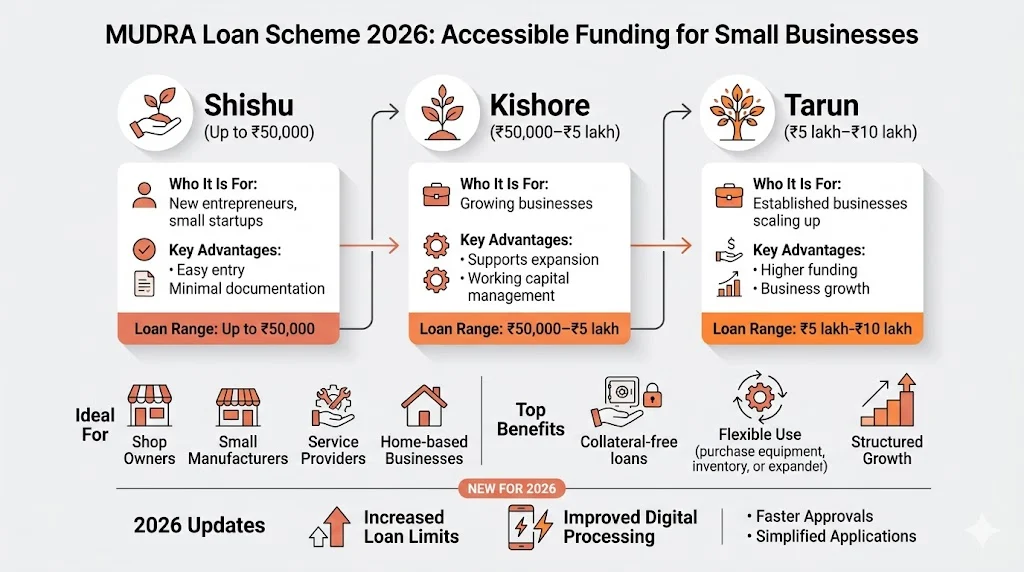

1) MUDRA Loan Scheme

MUDRA is one of the most popular schemes for small businesses. It supports people who want to start or expand their business by offering flexible and accessible funding options.

To make it easier to understand, here is a quick breakdown of who this scheme is for and its key advantages:

| Category | Who It Is For | Loan Range | Key Advantages |

|---|---|---|---|

| Shishu | New entrepreneurs, small startups | Up to ₹50,000 | Easy entry, minimal documentation |

| Kishore | Growing businesses | ₹50,000–₹5 lakh | Supports expansion and working capital |

| Tarun | Established businesses scaling up | ₹5 lakh–₹10 lakh | Higher funding for business growth |

This scheme is ideal for shop owners, small manufacturers, service providers, and even home-based businesses. One of the biggest advantages is that loans are usually collateral-free, which reduces risk for borrowers who do not have assets to pledge.

Another benefit is the flexibility in usage. Funds can be used for purchasing equipment, managing inventory, or expanding operations. The structured categories also help businesses grow step by step without taking unnecessary financial pressure.

In 2026, increased loan limits and improved digital processing have made MUDRA even more accessible. Faster approvals and simplified applications are encouraging more first-time entrepreneurs to take advantage of this scheme.

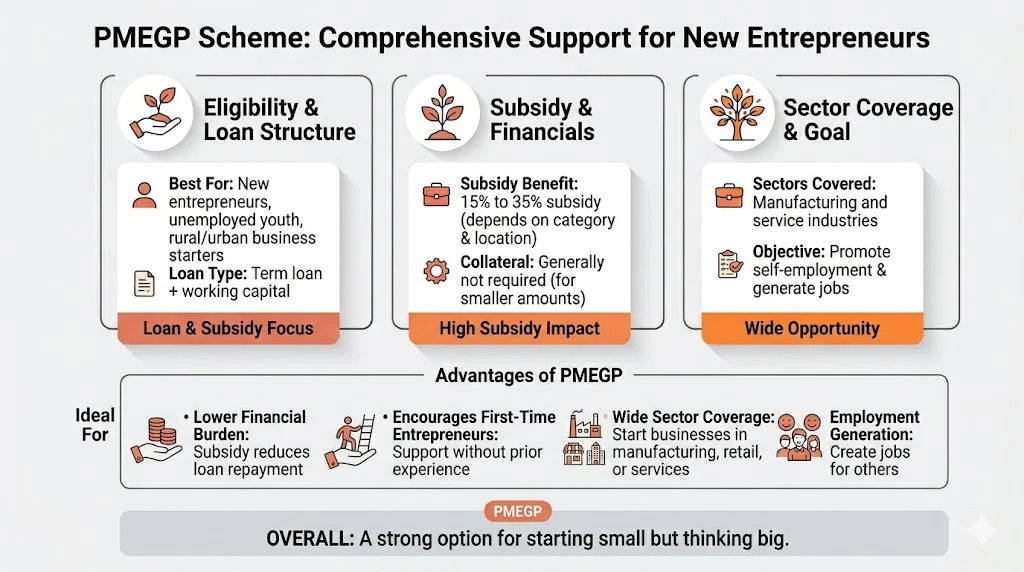

2) PMEGP Scheme

PMEGP is ideal for people who want to start a new business. It provides both loan and subsidy benefits, making it one of the most practical schemes for first-time entrepreneurs. To understand its value better, here is a quick breakdown:

| Category | Details |

|---|---|

| Best For | New entrepreneurs, unemployed youth, rural and urban business starters |

| Loan Type | Term loan + working capital |

| Subsidy Benefit | 15% to 35% subsidy depending on category and location |

| Sectors Covered | Manufacturing and service industries |

| Collateral | Generally not required for smaller loan amounts |

| Objective | Promote self-employment and generate jobs |

Advantages of PMEGP:

- Lower Financial Burden: The subsidy directly reduces the loan amount you need to repay, making it easier to manage finances in the early stages of business.

- Encourages First-Time Entrepreneurs: Even if you have no prior business experience, this scheme supports you with funding and guidance.

- Wide Sector Coverage: You can start businesses in manufacturing, retail, or services, giving flexibility based on your skills.

- Employment Generation: It not only helps you earn but also allows you to create jobs for others.

Overall, PMEGP is a strong option if you want to start small but think big, especially with limited capital.

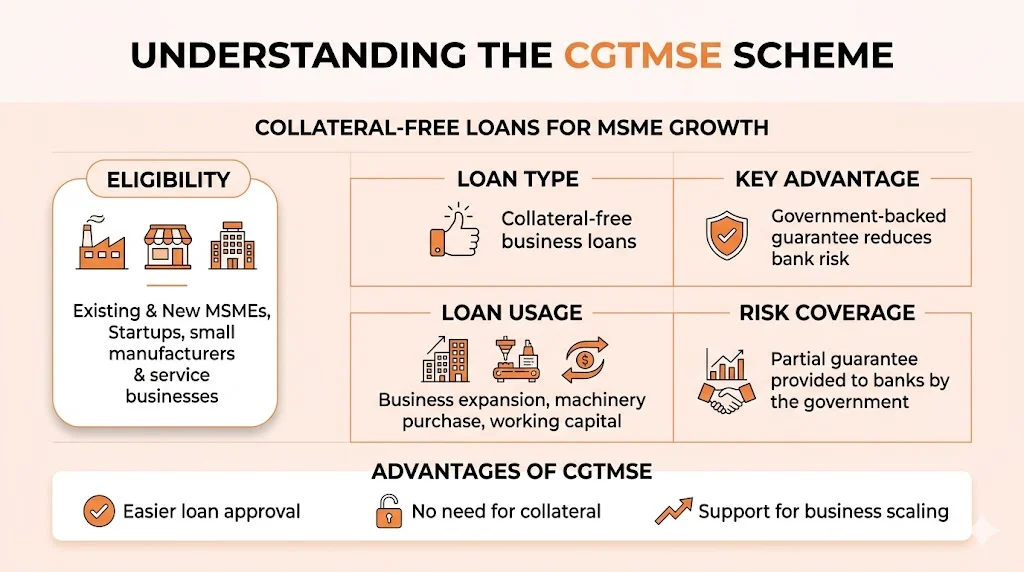

3) CGTMSE Scheme

CGTMSE is designed for MSMEs that need larger loans. It provides a government guarantee to banks, which reduces the risk for lenders and makes it easier for businesses to access funding without collateral.

Because of this guarantee, banks are more willing to approve loans for small and medium enterprises that may not have strong assets to pledge. This makes CGTMSE a powerful tool for business growth and expansion. Here is a quick breakdown to understand the scheme better:

| Category | Details |

|---|---|

| Best For | Existing MSMEs, small manufacturers, service businesses, startups |

| Loan Type | Collateral-free business loans |

| Key Advantage | Government-backed guarantee reduces bank risk |

| Loan Usage | Business expansion, machinery purchase, working capital |

| Eligibility | New and existing MSMEs with viable business plans |

| Risk Coverage | Partial guarantee provided to banks by the government |

Advantages of CGTMSE include easier loan approval, no need for collateral, and support for business scaling. It is especially useful for entrepreneurs who have strong business ideas but lack assets.

The scheme is ideal for businesses looking to expand operations, upgrade technology, or improve production capacity without financial pressure from collateral requirements.

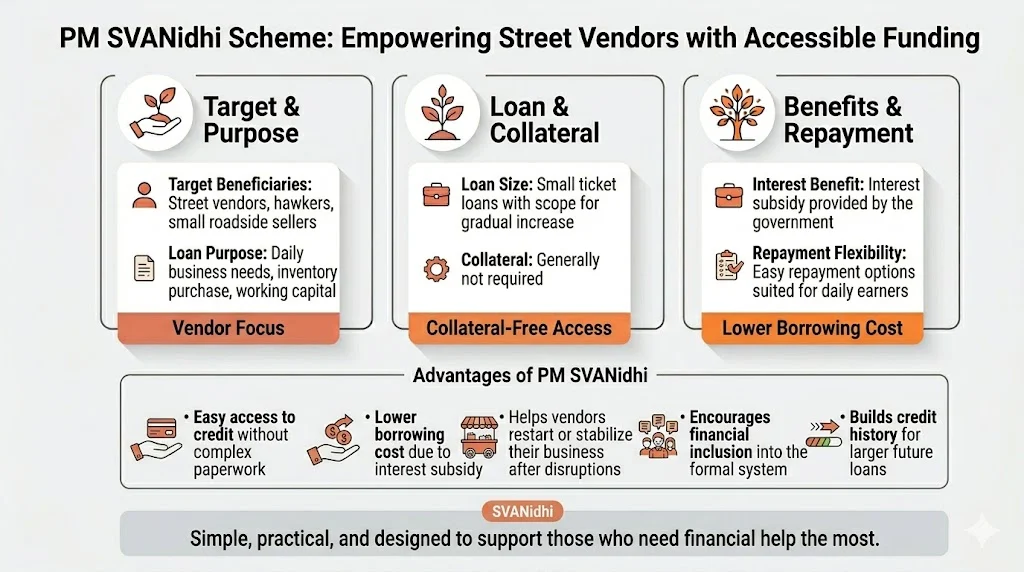

4) PM SVANidhi Scheme

This scheme is specially designed for street vendors who need quick and easy access to working capital. It provides small loans to help them run and expand their daily business without heavy financial pressure. To understand its value better, here is a quick breakdown:

| Feature | Details |

|---|---|

| Target Beneficiaries | Street vendors, hawkers, small roadside sellers |

| Loan Purpose | Daily business needs, inventory purchase, working capital |

| Loan Size | Small ticket loans with scope for gradual increase |

| Key Advantage | No collateral required |

| Interest Benefit | Interest subsidy provided by the government |

| Repayment Flexibility | Easy repayment options suited for daily earners |

Advantages of the scheme include:

- Easy access to credit without complex paperwork

- Lower borrowing cost due to interest subsidy

- Helps vendors restart or stabilize their business after disruptions

- Encourages financial inclusion by bringing vendors into the formal system

- Builds credit history, making it easier to get larger loans in the future

Many vendors have successfully used this scheme to improve their income and business stability. It is simple, practical, and designed to support those who need financial help the most.

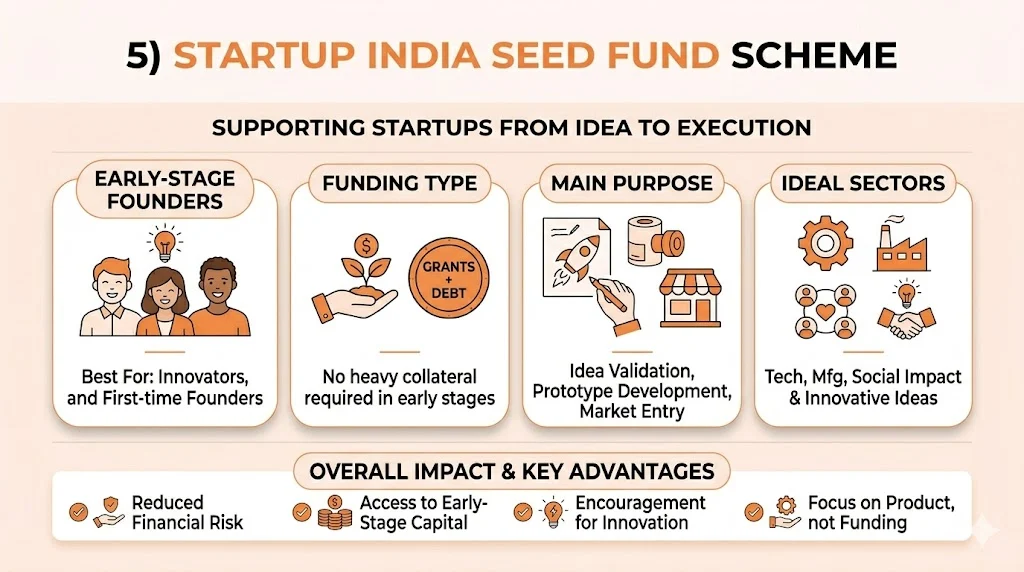

5) Startup India Seed Fund Scheme

This scheme supports startups in early stages. It provides both grants and debt funding, making it easier for founders to move from idea to execution without heavy financial pressure. To understand its value better, here is a quick breakdown:

| Category | Details |

|---|---|

| Best For | Early-stage startups, innovators, and first-time founders |

| Funding Type | Grants + Debt funding |

| Key Advantage | No heavy collateral required in early stages |

| Main Purpose | Support idea validation, prototype development, and market entry |

| Ideal Sectors | Technology, manufacturing, social impact, and innovative business ideas |

This scheme is especially useful for entrepreneurs who have strong ideas but lack initial capital. It helps startups move from idea stage to product development, which is often the most challenging phase due to limited funding options.

Some key advantages include reduced financial risk, access to early-stage capital, and encouragement for innovation. It also helps founders focus more on building their product rather than worrying about funding. Overall, the scheme plays a crucial role in strengthening India’s startup ecosystem by supporting new and innovative business ideas.

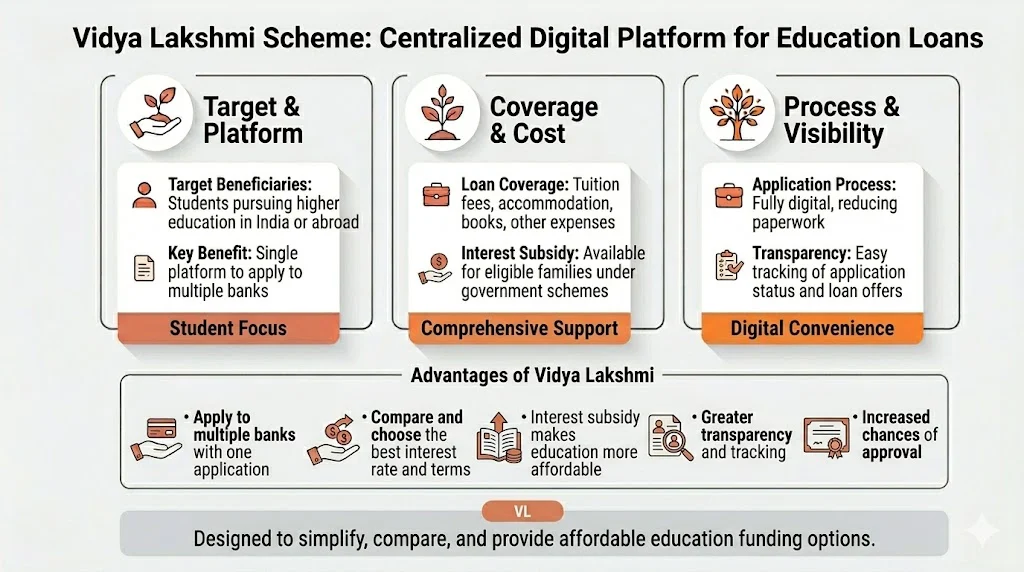

6) Vidya Lakshmi Scheme

This scheme is focused on students and is designed to simplify the process of getting an education loan through a centralized digital platform. It allows students to apply to multiple banks using a single application, saving both time and effort while increasing approval chances.

To better understand its value, here is a quick breakdown:

| Feature | Details |

|---|---|

| Who It Is For | Students pursuing higher education in India or abroad |

| Key Benefit | Single platform to apply to multiple banks |

| Loan Coverage | Tuition fees, accommodation, books, and other academic expenses |

| Interest Subsidy | Available for eligible families under government support schemes |

| Application Process | Fully digital, reducing paperwork and processing time |

| Transparency | Easy tracking of application status and loan offers |

One of the biggest advantages of this scheme is convenience. Instead of visiting multiple banks, students can compare loan options in one place. This helps in choosing the best interest rate and repayment terms.

Additionally, the interest subsidy feature makes education more affordable for students from economically weaker sections. Overall, this scheme reduces financial stress and makes higher education more accessible and manageable.

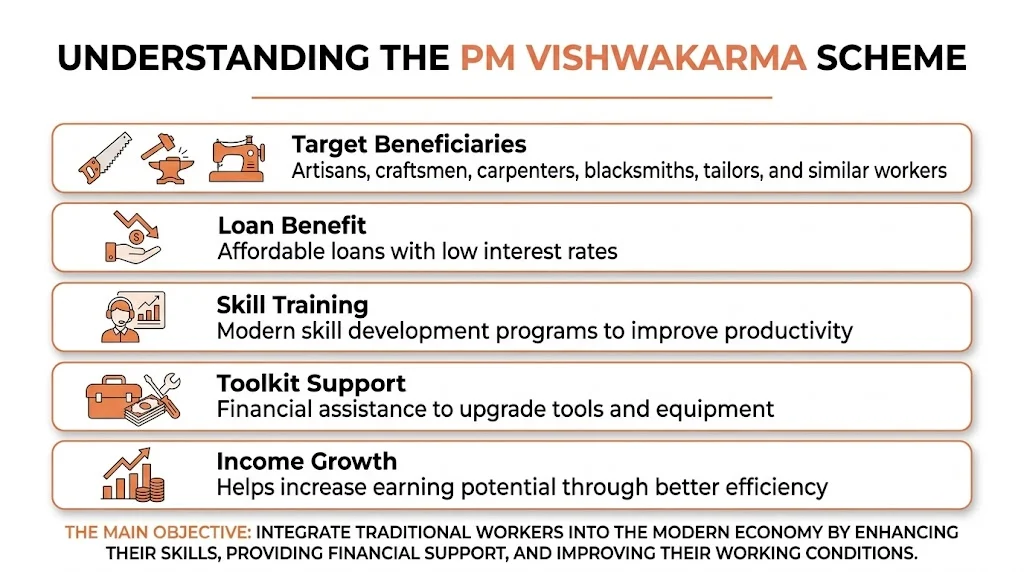

7) PM Vishwakarma Scheme

This scheme supports traditional workers and artisans by offering low interest loans along with skill development training. It is designed to strengthen the livelihoods of individuals engaged in crafts, trades, and manual professions. To better understand its value, here is a quick breakdown:

| Feature | Details |

|---|---|

| Target Beneficiaries | Artisans, craftsmen, carpenters, blacksmiths, tailors, and similar workers |

| Loan Benefit | Affordable loans with low interest rates |

| Skill Training | Modern skill development programs to improve productivity |

| Toolkit Support | Financial assistance to upgrade tools and equipment |

| Income Growth | Helps increase earning potential through better efficiency |

The scheme also includes toolkit incentives, which allow workers to upgrade their equipment and improve the quality of their work. This directly impacts their productivity and income.

Overall, the main objective is to integrate traditional workers into the modern economy by enhancing their skills, providing financial support, and improving their working conditions.

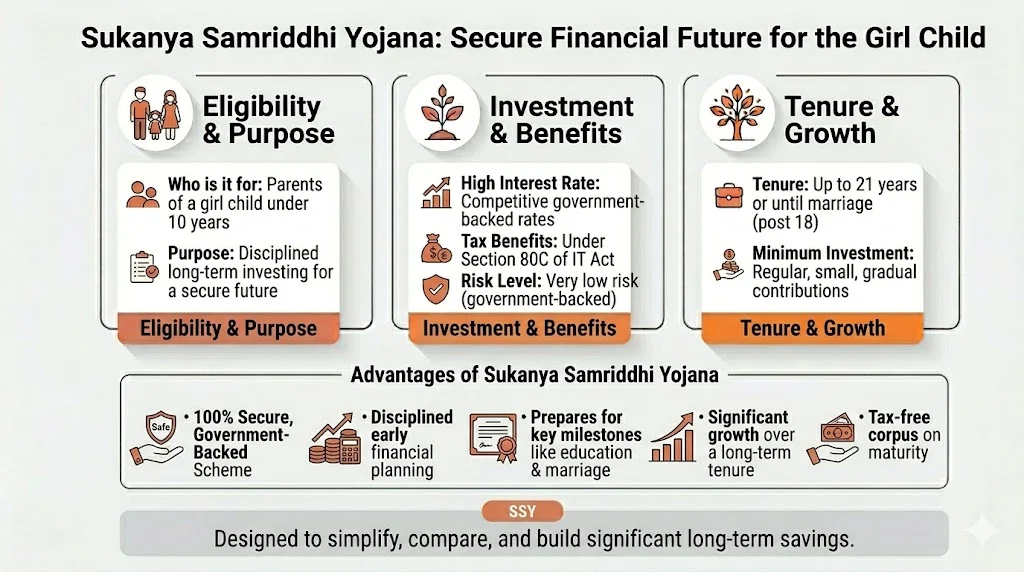

8) Sukanya Samriddhi Yojana

This is a savings scheme for the girl child that helps parents build a secure financial future through disciplined investing. It offers attractive interest rates along with tax benefits, making it one of the most reliable long-term savings options in India. To understand its value better, here is a quick breakdown:

| Feature | Details |

|---|---|

| Who is it for | Parents or guardians of a girl child below 10 years of age |

| Investment Type | Long-term savings scheme |

| Key Advantages | High interest rate, tax benefits under Section 80C, safe government-backed |

| Investment Tenure | Up to 21 years or until marriage after 18 years |

| Minimum Investment | Low yearly contribution required |

| Risk Level | Very low, as it is backed by the government |

Parents can invest regularly in small amounts, which gradually grows into a significant corpus over time. The scheme encourages early financial planning for important milestones like education and marriage.

Although it is not a loan scheme, it plays a crucial role in financial security. It ensures that families are prepared for future expenses without depending on external borrowing.

Quick Comparison Of Major Schemes

| Scheme Name | Benefit Type | Best For | Key Advantage |

|---|---|---|---|

| MUDRA | Business Loan | Small businesses | No collateral |

| PMEGP | Loan + Subsidy | New entrepreneurs | Lower repayment burden |

| CGTMSE | Guaranteed Loan | MSMEs | Easy approval |

| SVANidhi | Small Loan | Street vendors | Interest subsidy |

| Startup Fund | Grant + Loan | Startups | Early stage support |

| Vidya Lakshmi | Education Loan | Students | Digital application |

This table helps you quickly compare and choose the right scheme.

Public Opinion And Real Usage (Data From X)

People are actively using these schemes. Many small business owners have started shops using MUDRA loans. Street vendors have improved their income through SVANidhi.

Young entrepreneurs are exploring startup funding schemes. Students are using digital platforms for education loans. At the same time, some people face challenges like approval delays or repayment pressure. Overall, the sentiment is positive because these schemes solve real problems.

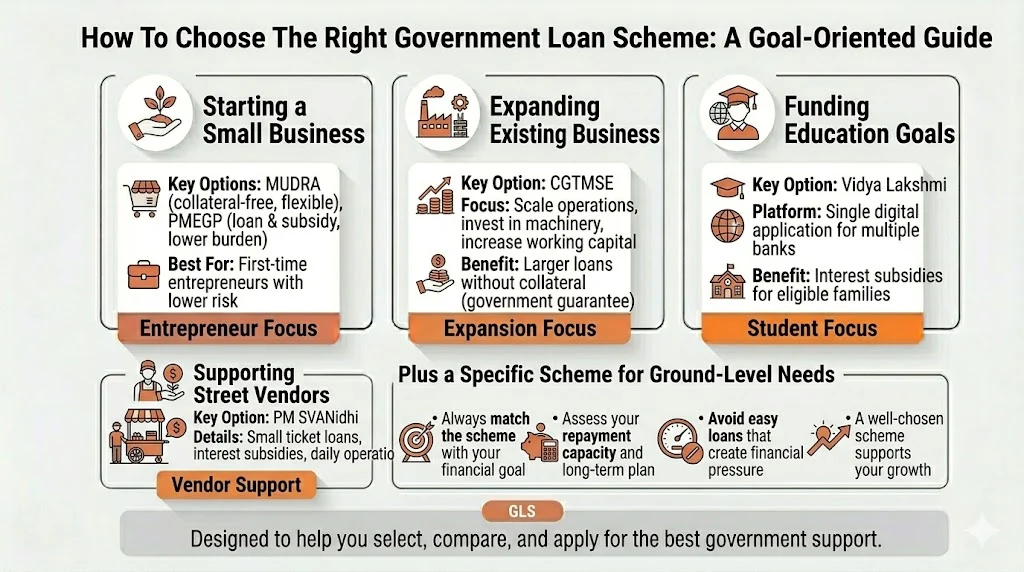

How To Choose The Right Government Loan Scheme

Choosing the right scheme depends on your goal.

- Starting a Small Business: If you are planning to start a small business, MUDRA and PMEGP are two of the most practical options. MUDRA offers collateral free loans with flexible categories based on your business stage, while PMEGP provides a combination of loan and subsidy, reducing your repayment burden. These schemes are ideal for first time entrepreneurs who need financial support with lower risk.

- Expanding an Existing Business: If you already run a business and want to scale operations, invest in machinery, or increase working capital, CGTMSE is a strong choice. It allows you to access larger loans without collateral because the government provides a guarantee to banks. This makes it easier to secure funding and grow your business faster.

- Supporting Street Vendors: If you are a street vendor or small daily earner, PM SVANidhi is specifically designed for you. It offers small ticket loans with interest subsidies, helping you manage daily operations and improve income stability. The scheme is simple, accessible, and focused on real ground level needs.

- Funding Education Goals: If you are a student looking to finance your education, Vidya Lakshmi is a smart option. It provides a single digital platform where you can apply to multiple banks, saving time and effort. It also offers interest subsidies for eligible families, making higher education more affordable.

- Choosing the Right Scheme Smartly: Always match the scheme with your financial goal, repayment capacity, and long term plan. Avoid choosing a loan just because it is easily available. A well chosen scheme can support your growth, while a wrong choice can create financial pressure.

Important Things To Check Before Applying

Before applying for any loan, follow this smart checklist to make better financial decisions:

- Check Eligibility First: Always review the eligibility criteria carefully. Each scheme has different requirements, and applying without meeting them can lead to rejection and wasted time.

- Understand Repayment Terms: Go through interest rates, tenure, and repayment structure. Knowing these details helps you avoid surprises and plan your finances effectively.

- Calculate Your EMI: Use an EMI calculator to estimate your monthly payments. This ensures the loan fits comfortably within your budget.

- Prepare All Documents: Keep identity proof, income proof, and other required documents ready. This speeds up approval and reduces delays.

- Assess Your Repayment Capacity: Do not borrow more than you can repay. Always consider your current income, expenses, and future financial commitments.

- Compare Multiple Options: Explore different schemes and lenders to find the best interest rates and benefits.

Following these steps can help you choose the right loan and avoid financial stress.

Common Mistakes To Avoid

- Applying Without Understanding The Scheme: Many applicants rush into loan applications without fully understanding the scheme details. This often leads to rejection or choosing the wrong loan product. Always read eligibility criteria, benefits, and conditions carefully before applying.

- Borrowing More Than Required: Taking a higher loan amount than necessary may seem helpful initially, but it increases your repayment burden over time. Always calculate your exact financial need and borrow only what you can comfortably repay.

- Ignoring Interest Rates And Hidden Charges: Many borrowers focus only on loan approval and ignore interest rates, processing fees, and hidden costs. These factors significantly impact your total repayment amount. Always compare options and understand the complete cost of borrowing.

- Not Checking Repayment Capacity: Failing to assess your monthly income and expenses can lead to repayment stress. Before applying, calculate your EMI and ensure it fits within your budget without affecting essential expenses.

- Submitting Incomplete Or Incorrect Documents: Incomplete or incorrect documentation can delay approval or lead to rejection. Double check all required documents and ensure accuracy before submission.

Avoiding these common mistakes can significantly improve your chances of loan approval and help you manage your finances more effectively.

Future Of Government Loan Schemes

Government schemes will continue to grow in the coming years. More digital integration will make processes faster. Loan limits may increase further. More sectors will be covered.

Focus on women empowerment and rural development will increase. These schemes will play a major role in India’s economic growth.

Blog Post Conclusion

In my view, government loan schemes in 2026 are not just financial tools. They are real opportunities for growth and stability. Whether you are a small business owner, a student, or someone planning for the future, there is a scheme designed for you.

But success depends on how you use these schemes. You need to choose wisely, understand terms clearly, and manage repayment responsibly. Taking a loan is a financial commitment, so it requires planning.

If you approach these schemes with the right mindset, they can help you build a strong financial foundation. The system is improving, opportunities are growing, and the right decision today can create long term benefits for you and your family.

Related Posts :

Share This Post