Best Government Multibagger Stocks 2026: Hidden PSU Gems That Can Deliver Massive Returns In The Next 5 Years

Best Government Multibagger Stocks 2026: Hidden PSU Gems That Can Deliver Massive Returns In The Next 5 Years

If you are watching the Indian stock market closely, then one thing is becoming very clear in 2026. PSU stocks are no longer slow moving dividend stocks. They are now turning into powerful wealth creation opportunities for long term investors. Many government companies are showing strong earnings growth, large order books, and consistent performance across sectors like defence, railways, power, and metals.

Investors are actively searching for the best government multibagger stocks 2026 because the opportunity looks real and not just hype. Earlier, these stocks were ignored due to low growth and policy risks. But now the story has changed. Strong government spending, self reliance push, and infrastructure development are driving growth in PSU companies. Retail investors are also showing strong interest and building PSU focused portfolios.

In this blog post we will see which sectors are leading this transformation what PSU stocks have multibagger potential? what are the key growth triggers & how you can evaluate these stocks smartly.

This is not just a list. This is a complete guide to help you think like a long term investor in 2026. I promise that you will get lot more information than other articles on the internet so lets get started…

Table of Contents

Why PSU Stocks Are Booming In 2026

The biggest reason behind PSU growth is government spending. India is investing heavily in infrastructure, defence, and renewable energy. PSU companies are the main beneficiaries of these projects. They receive large contracts and long term visibility.

Market data shows that PSU market capitalization has crossed around ₹69 lakh crore. Earnings growth has also improved strongly in the last few years. Many PSUs are now delivering consistent profits and better return ratios.

Another important factor is valuation rerating. Earlier PSU stocks were available at very low valuations. Now investors are willing to pay higher valuations because of strong performance and growth visibility. This shift from discount to premium is creating wealth for investors.

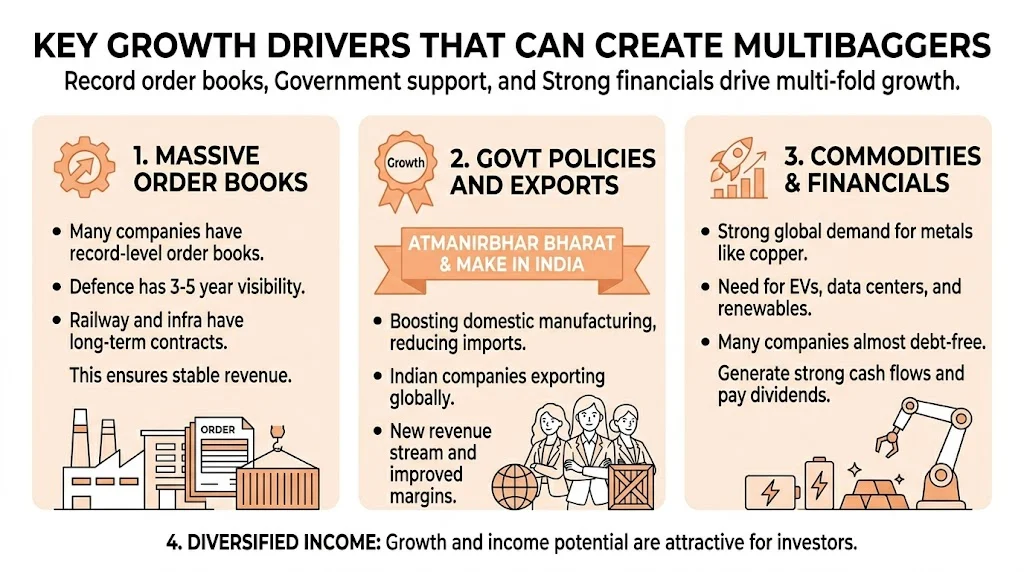

Key Growth Drivers That Can Create Multibaggers

1. Massive Order Books

Many PSU companies have record level order books. Defence companies have visibility for the next 3 to 5 years. Railway and infrastructure companies also have long term contracts. This ensures stable revenue growth.

2. Government Policies And Support

Government policies like Atmanirbhar Bharat and Make in India are boosting domestic manufacturing. Defence imports are reducing. Local companies are getting more opportunities.

3. Export Opportunities

Indian defence and engineering companies are now exporting products globally. This adds a new revenue stream and improves margins.

4. Commodity Cycles

Metals like copper are seeing strong global demand. Electric vehicles, data centers, and renewable energy need large amounts of copper. This creates long term growth for metal PSUs.

5. Strong Financials

Many PSU companies are almost debt free. They generate strong cash flows and pay dividends. This makes them attractive for both growth and income investors.

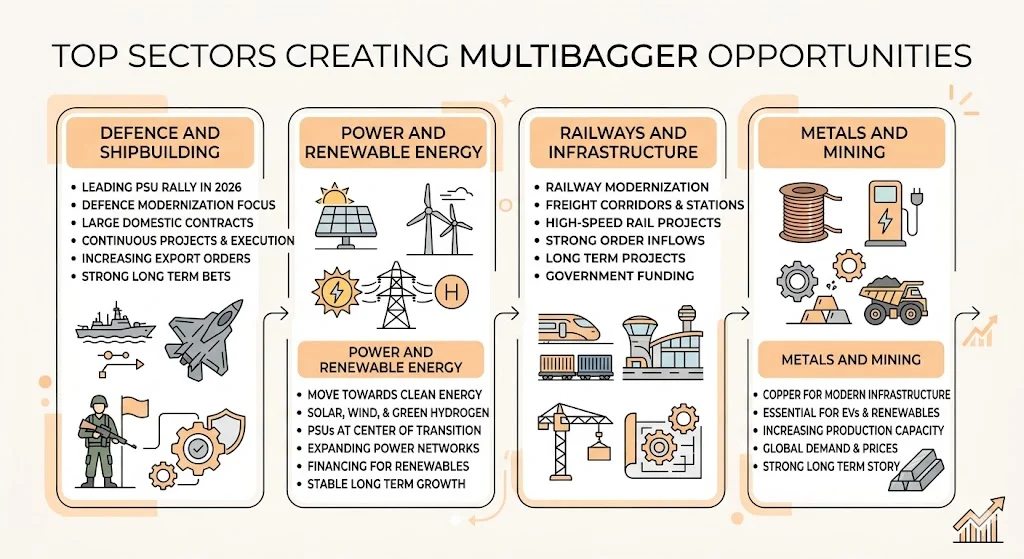

Top Sectors Creating Multibagger Opportunities

1) Defence And Shipbuilding

This sector is leading the PSU rally in 2026. Government focus on defence modernization is very strong. Large contracts are being awarded to domestic companies. Companies are getting continuous projects. Their execution capability is improving. Export orders are also increasing. This makes defence stocks strong long term bets.

2) Power And Renewable Energy

India is moving towards clean energy. Solar, wind, and green hydrogen projects are increasing. PSU companies are at the center of this transition. Power generation and transmission companies are expanding their networks. Financing companies are supporting renewable projects. This sector has stable and long term growth.

3) Railways And Infrastructure

Railway modernization is creating huge opportunities. Freight corridors, station redevelopment, and high speed rail projects are growing. Companies involved in execution and financing are getting strong order inflows. These projects are long term and funded by the government.

4) Metals And Mining

Copper is becoming very important for modern infrastructure. Electric vehicles and renewable energy require copper. Metal PSU companies are increasing production capacity. Global demand is supporting prices. This creates a strong long term story.

Also Read: List Of Dividend Paying FMCG Stocks In India 2026

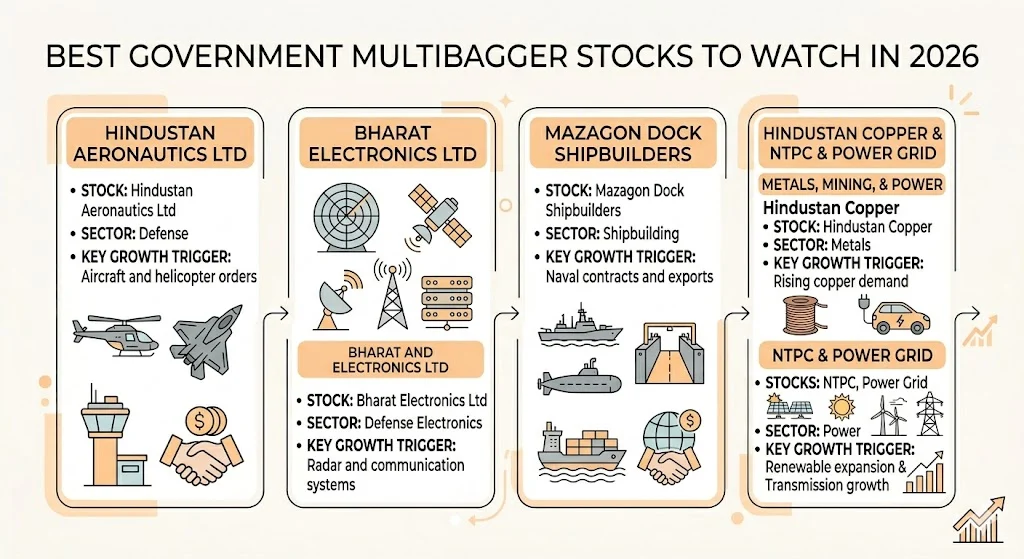

Best Government Multibagger Stocks To Watch In 2026

Below is a carefully structured list of PSU stocks based on sector strength and growth potential.

| Stock Name | Sector | Key Growth Trigger |

|---|---|---|

| Hindustan Aeronautics Ltd | Defense | Aircraft and helicopter orders |

| Bharat Electronics Ltd | Defense Electronics | Radar and communication systems |

| Mazagon Dock Shipbuilders | Shipbuilding | Naval contracts and exports |

| Garden Reach Shipbuilders | Shipbuilding | Warship projects |

| Rail Vikas Nigam Ltd | Railways | Infrastructure execution |

| Hindustan Copper | Metals | Rising copper demand |

| NTPC | Power | Renewable expansion |

| Power Grid | Power | Transmission growth |

These companies are not just popular. They have strong business fundamentals and growth visibility. Detailed Explanation Of Each PSU Stock

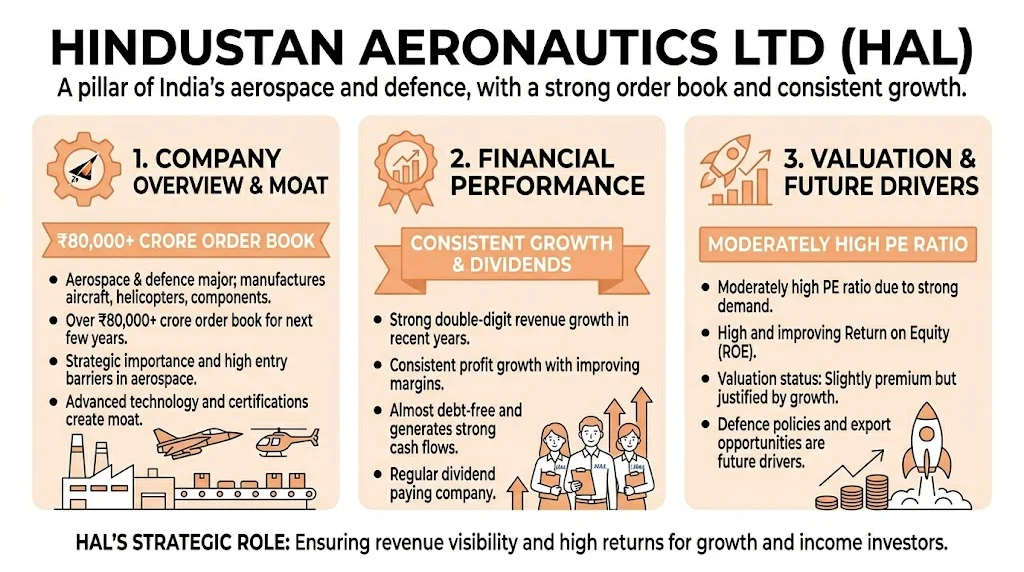

Hindustan Aeronautics Ltd

Hindustan Aeronautics is one of the strongest defence PSU companies in India. It manufactures aircraft, helicopters, and aerospace components for the Indian armed forces. The company has a massive order book of over ₹80,000 crore, which provides strong revenue visibility for the next few years.

Its revenue growth has been consistent, and profit margins are improving due to better execution and higher value contracts. The company is almost debt free and generates strong cash flows.

The moat of HAL lies in its strategic importance and high entry barriers. Aerospace manufacturing requires advanced technology, certifications, and long development cycles. Very few companies can compete in this space, which gives HAL a strong competitive advantage.

Also Read: Best Penny Stocks With High Growth Potential: 10 Hidden Multibaggers For 2030 You Should Watch

| Financial Metric | Details (Recent Trends) |

|---|---|

| Revenue Growth | Strong double digit growth in recent years |

| Profit Growth | Consistent increase with improving margins |

| PE Ratio | Moderately high due to strong demand |

| Dividend Yield | Yes, regular dividend paying company |

| Debt Level | Very low, almost debt free |

| Return on Equity (ROE) | High and improving |

| Order Book Strength | ₹80,000+ crore visibility |

| Valuation Status | Slightly premium but justified by growth |

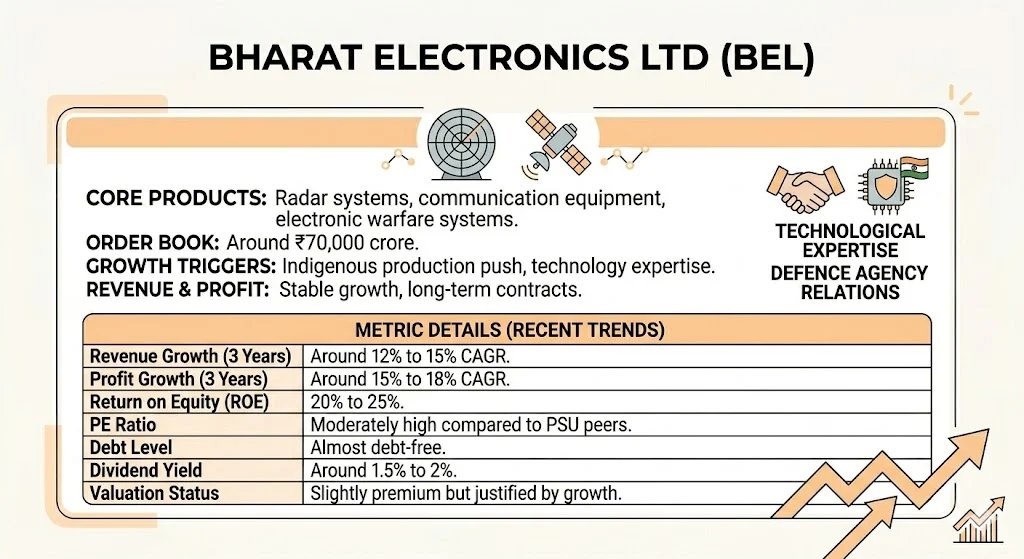

Bharat Electronics Ltd

Bharat Electronics is a leading defence electronics company. It manufactures radar systems, communication equipment, and electronic warfare systems. The company has an order book of around ₹70,000 crore and continues to receive new contracts regularly. It has strong revenue growth, high return on equity, and stable margins.

The company has a strong balance sheet with minimal debt and consistent dividend payouts. Its moat comes from its technological expertise and long term relationships with defence agencies. It also benefits from the government’s push for indigenous defence production.

| Metric | Details (Recent Trends) |

|---|---|

| Revenue Growth (3 Years) | Around 12% to 15% CAGR |

| Profit Growth (3 Years) | Around 15% to 18% CAGR |

| Return on Equity (ROE) | 20% to 25% |

| PE Ratio | Moderately high compared to PSU peers |

| Debt Level | Almost debt free |

| Dividend Yield | Around 1.5% to 2% |

| Valuation Status | Slightly premium but justified by growth |

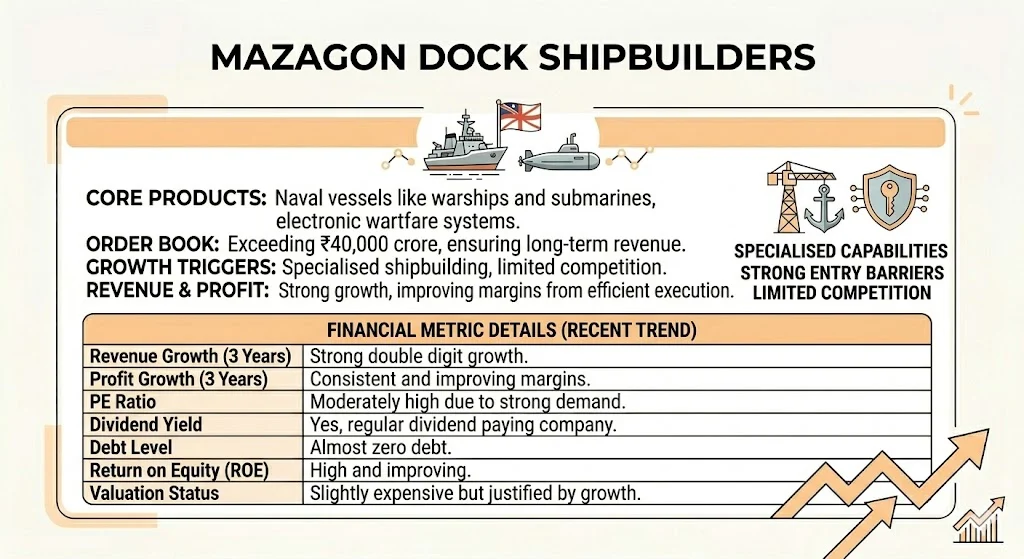

Mazagon Dock Shipbuilders

Mazagon Dock is a key player in shipbuilding, especially for naval vessels like submarines and warships. The company has an order book exceeding ₹40,000 crore, which ensures long term revenue visibility. It has shown strong profit growth and improving margins due to efficient execution.

The company is debt free and has strong cash reserves. Its moat lies in its specialized shipbuilding capabilities and limited competition. Building submarines and warships requires high technical expertise and infrastructure, which creates strong entry barriers.

| Financial Metric | Details (Recent Trend) |

|---|---|

| Revenue Growth (3 Years) | Strong double digit growth |

| Profit Growth (3 Years) | Consistent and improving margins |

| PE Ratio | Moderately high due to strong demand |

| Dividend Yield | Yes, regular dividend paying company |

| Debt Level | Almost zero debt |

| Return on Equity (ROE) | High and improving |

| Valuation Status | Slightly expensive but justified by growth |

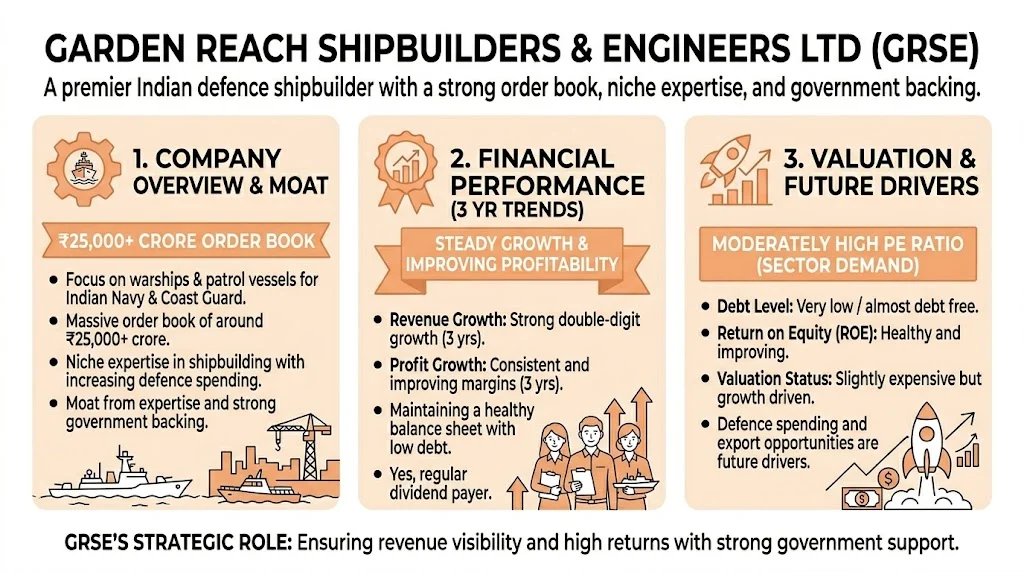

Garden Reach Shipbuilders

Garden Reach Shipbuilders focuses on building warships and patrol vessels for the Indian Navy and Coast Guard. The company has an order book of around ₹25,000 crore and continues to receive new defence contracts. It has shown steady revenue growth and improving profitability.

The company maintains a healthy balance sheet with low debt. Its moat comes from its niche expertise in shipbuilding and strong government backing. It also benefits from increasing defence spending and export opportunities.

| Financial Metric | Details (Recent Trends) |

|---|---|

| Revenue Growth (3 Years) | Strong double digit growth |

| Profit Growth (3 Years) | Consistent and improving margins |

| PE Ratio | Moderately high due to sector demand |

| Dividend Payment | Yes, regular dividend payer |

| Debt Level | Very low / almost debt free |

| Return on Equity (ROE) | Healthy and improving |

| Valuation Status | Slightly expensive but growth driven |

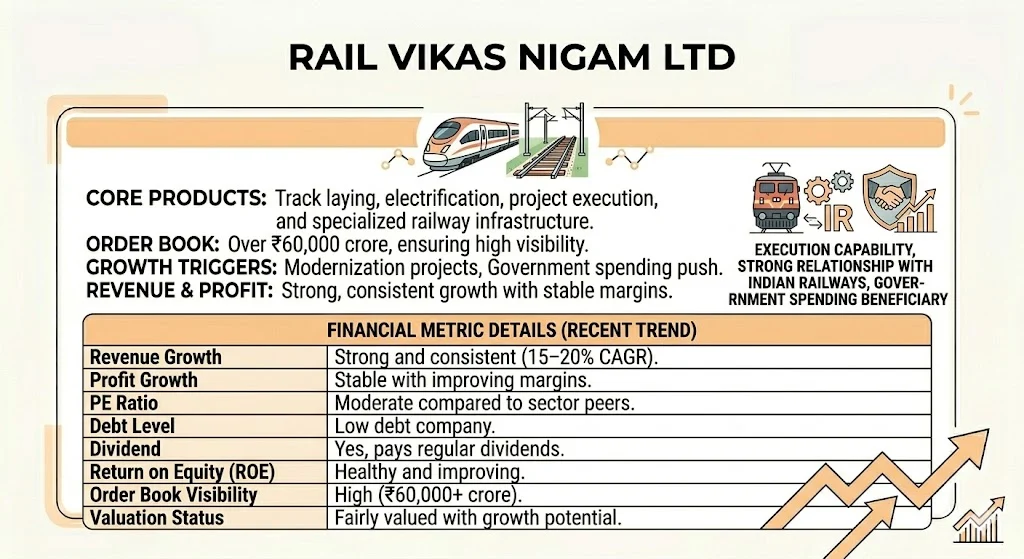

Rail Vikas Nigam Ltd

Rail Vikas Nigam is involved in railway infrastructure development, including track laying, electrification, and project execution. The company has a strong order book of over ₹60,000 crore. It has shown consistent revenue growth and stable margins.

The company operates with low debt and generates steady cash flows. Its moat lies in its execution capability and strong relationship with Indian Railways. It benefits directly from government spending on railway modernization.

| Financial Metric | Details (Recent Trends) |

|---|---|

| Revenue Growth | Strong and consistent (15–20% CAGR) |

| Profit Growth | Stable with improving margins |

| PE Ratio | Moderate compared to sector peers |

| Debt Level | Low debt company |

| Dividend | Yes, pays regular dividends |

| Return on Equity (ROE) | Healthy and improving |

| Order Book Visibility | High (₹60,000+ crore) |

| Valuation Status | Fairly valued with growth potential |

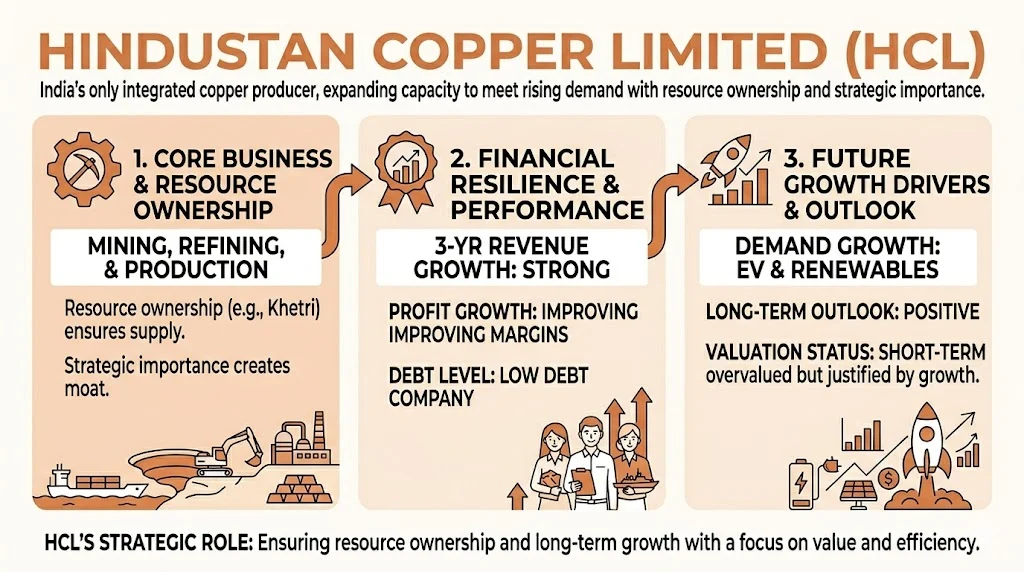

Hindustan Copper

Hindustan Copper is the only integrated copper producer in India. It is involved in mining, refining, and production of copper. The company is expanding its production capacity to meet rising demand. Its revenue and profits are closely linked to global copper prices.

The company has low debt and improving financial performance. Its moat comes from its resource ownership and strategic importance. Copper demand is expected to grow due to electric vehicles and renewable energy, which supports long term growth.

| Financial Metric | Details (Recent Trends) |

|---|---|

| Revenue Growth | Strong growth in last 3 years |

| Profit Growth | Improving margins and rising profits |

| PE Ratio | Moderately high due to future expectations |

| Debt Level | Low debt company |

| Dividend | Pays dividend but not very high yield |

| Return on Equity (ROE) | Improving steadily |

| Valuation Status | Slightly overvalued in short term |

| Long Term Outlook | Positive due to copper demand growth |

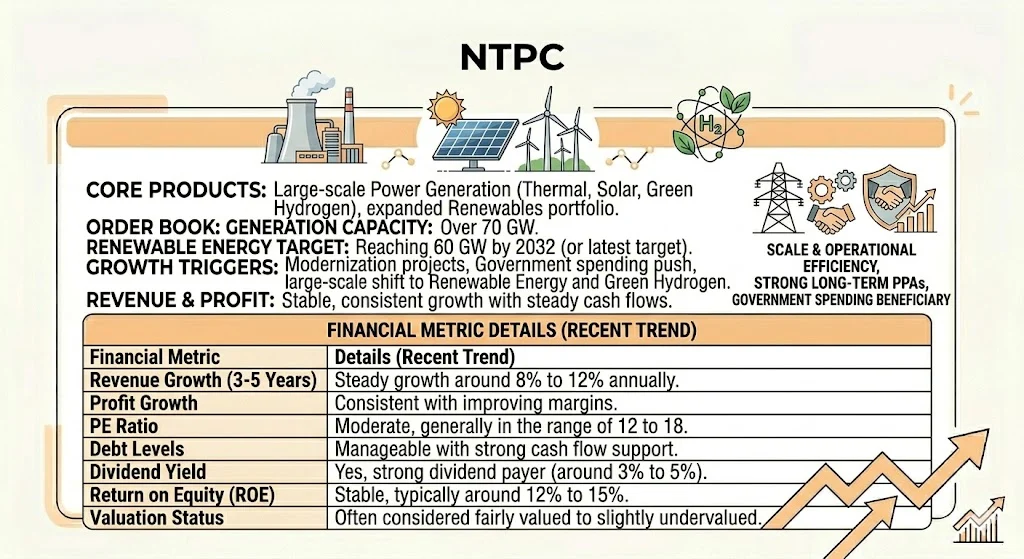

NTPC

NTPC is India’s largest power generation company. It is expanding into renewable energy, including solar and green hydrogen projects. The company has stable revenue growth and strong cash flows. It maintains a healthy balance sheet with manageable debt levels.

Its moat lies in its scale, operational efficiency, and long term power purchase agreements. These agreements ensure predictable revenue and reduce risk.

| Financial Metric | Details (Recent Trends) |

|---|---|

| Revenue Growth (3-5 Years) | Steady growth around 8% to 12% annually |

| Profit Growth | Consistent with improving margins |

| PE Ratio | Moderate, generally in the range of 12 to 18 |

| Dividend Yield | Yes, strong dividend payer (around 3% to 5%) |

| Debt Levels | Manageable with strong cash flow support |

| Return on Equity (ROE) | Stable, typically around 12% to 15% |

| Valuation Status | Often considered fairly valued to slightly undervalued |

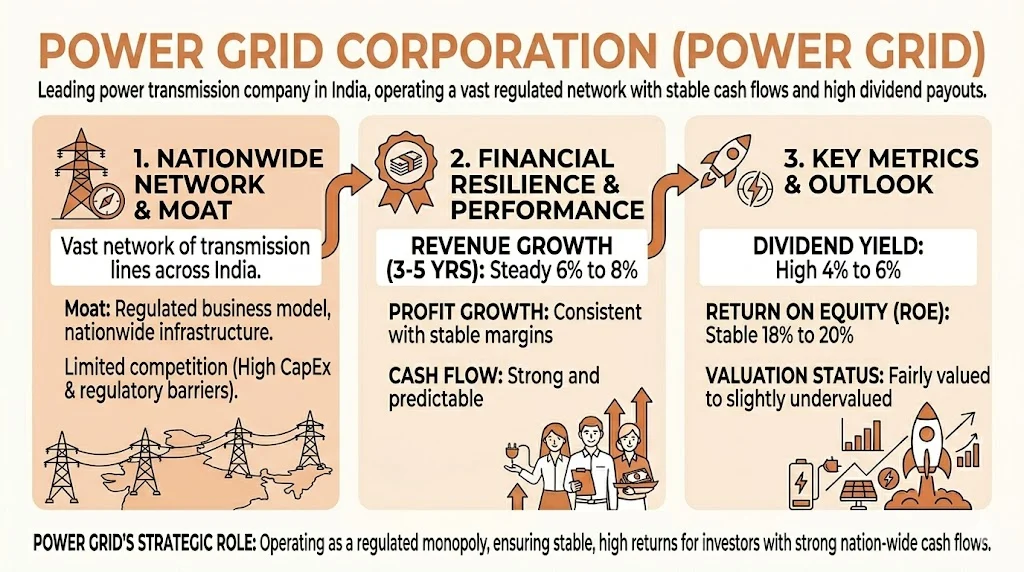

Power Grid Corporation

Power Grid is a leading power transmission company in India. It operates a vast network of transmission lines across the country. The company has stable earnings and consistent dividend payouts. It has strong financials with steady cash flows.

The moat of Power Grid comes from its regulated business model and nationwide infrastructure network. It has very limited competition due to high capital requirements and regulatory barriers.

| Financial Metric | Details (Recent Trends) |

|---|---|

| Revenue Growth (3-5 Years) | Steady growth around 6% to 8% |

| Profit Growth | Consistent growth with stable margins |

| PE Ratio | Moderate, generally in 10 to 15 range |

| Dividend Yield | High, around 4% to 6% |

| Debt Levels | Manageable due to regulated returns |

| Return on Equity (ROE) | Stable around 18% to 20% |

| Cash Flow | Strong and predictable |

| Valuation Status | Fairly valued to slightly undervalued |

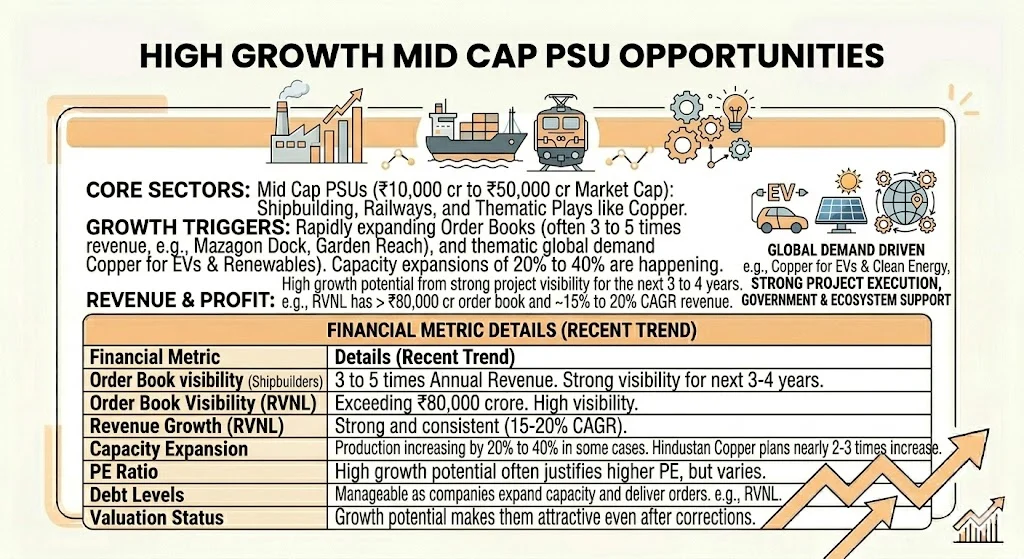

High Growth Mid Cap PSU Opportunities

Most investors focus only on large companies. But data shows that real multibagger returns often come from mid cap stocks, especially those with market capitalizations between ₹10,000 crore to ₹50,000 crore, where growth potential is still high.

Companies like Mazagon Dock and Garden Reach Shipbuilders have delivered strong returns in recent years, with some stocks rising more than 200% to 400% in the last 2 to 3 years. Their order books are expanding rapidly, often 3 to 5 times their annual revenue, which gives strong visibility for the next 3 to 4 years. Capacity expansion is also happening, with production capabilities increasing by 20% to 40% in some cases.

Rail Vikas Nigam is another example. It benefits from railway projects and infrastructure growth, with an order book exceeding ₹80,000 crore and consistent revenue growth of around 15% to 20% annually. Even after corrections of 20% to 30% from peak levels, it still has long term potential due to strong project execution and government support.

Hindustan Copper is a thematic play. India’s copper demand is expected to grow at 6% to 8% CAGR, while global demand is projected to increase significantly due to electric vehicles and renewable energy. The company is also planning to increase its production capacity by nearly 2 to 3 times over the next few years. If the global copper demand continues, this stock can perform strongly.

Stable PSU Compounders With Upside

Some PSU stocks may not give very fast returns but they offer stability with growth. NTPC is focusing on renewable energy. Power Grid is expanding transmission networks. These companies have strong balance sheets and predictable earnings. Such stocks can form the core of a portfolio. They provide stability while high growth stocks add returns.

Public Sentiment And Retail Investor Buzz (Data Taken From X)

Retail investors are showing strong interest in PSU stocks. Social media platforms are full of discussions about defence and copper themes. Many investors are calling shipbuilding companies as future multibaggers. Some are comparing defence stocks to find the best pick.

There is also strong interest in copper due to global demand. At the same time, some investors are cautious due to high valuations. This mix of excitement and caution is healthy. It shows that investors are becoming more aware and selective.

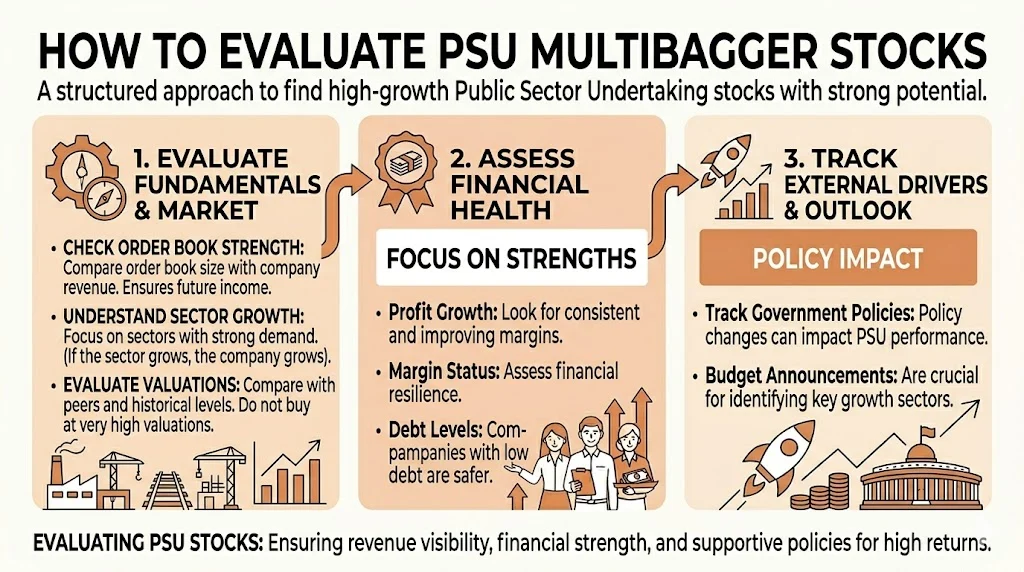

How To Evaluate PSU Multibagger Stocks

- Check Order Book Strength: A strong order book ensures future revenue. Compare order book size with company revenue.

- Analyze Financial Health: Look at profit growth, margins, and debt levels. Companies with low debt are safer.

- Understand Sector Growth: If the sector is growing, the company will also grow. Focus on sectors with strong demand.

- Track Government Policies: Policy changes can impact PSU performance. Budget announcements are important.

- Evaluate Valuations: Do not buy stocks at very high valuations. Compare with peers and historical levels.

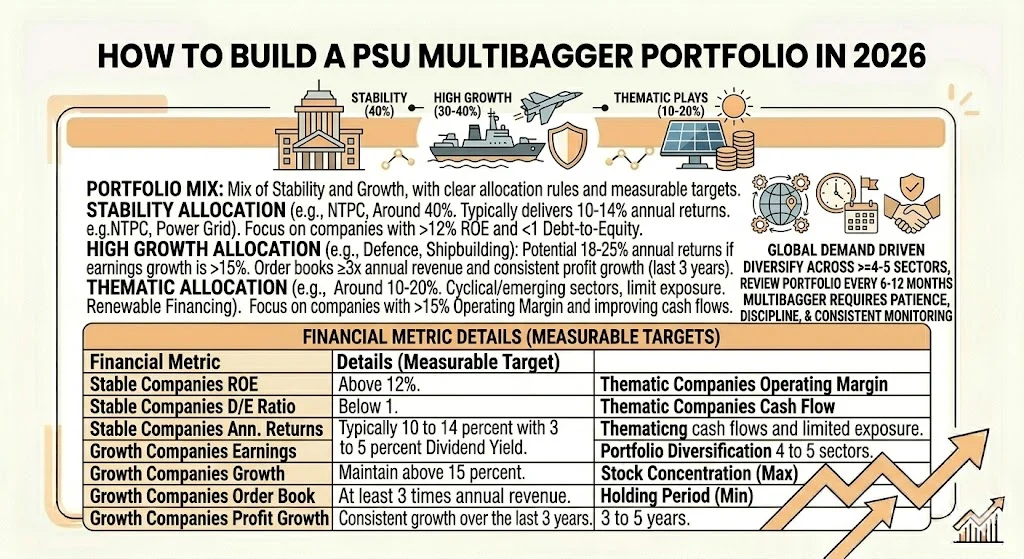

How To Build A PSU Multibagger Portfolio In 2026

A smart portfolio should have a mix of stability and growth, backed by clear allocation rules and measurable targets.

You can allocate around 40 percent in stable companies like NTPC and Power Grid. These companies typically deliver 10 to 14 percent annual returns with dividend yields of 3 to 5 percent. Ensure that these stocks have a return on equity above 12 percent and a debt to equity ratio below 1 for financial safety.

Around 30 to 40 percent can be invested in high growth sectors like defence and shipbuilding. These stocks can potentially deliver 18 to 25 percent annual returns if earnings growth remains above 15 percent. Focus on companies with order books at least 3 times their annual revenue and consistent profit growth over the last 3 years.

The remaining 10 to 20 percent can be allocated to thematic plays like copper or renewable financing. These are cyclical or emerging sectors, so limit exposure and track global demand trends. Look for companies with operating margins above 15 percent and improving cash flows.

Always diversify across at least 4 to 5 sectors to reduce concentration risk. Avoid allocating more than 10 percent to a single stock. Hold investments for at least 3 to 5 years. Review your portfolio every 6 to 12 months and rebalance if any stock exceeds 25 percent of total allocation. Multibagger returns require patience, discipline, and consistent monitoring.

Risks You Should Not Ignore

- Policy Risks: Government decisions can impact PSU companies. Delays or changes can affect growth.

- Execution Risks: Infrastructure projects can face delays. This can impact earnings.

- Commodity Price Risks: Metal companies depend on global prices. Price fluctuations can affect profits.

- Valuation Risks: Some PSU stocks are already expensive. Buying at high prices can reduce returns.

- Market Corrections: After strong rallies, corrections are normal. Investors should be prepared for volatility.

Future Outlook For PSU Stocks

The future of PSU stocks looks strong in 2026 and beyond. Government focus on infrastructure and self reliance will continue. Defence exports are expected to grow. Renewable energy investments will increase. Railway projects will expand further.

Commodity demand will also remain strong due to global trends. All these factors support long term growth. But not every PSU will become a multibagger. Investors need to select the right companies with strong fundamentals.

My Final Words

In my view, PSU stocks are going through a major transformation. What used to be slow and ignored is now becoming a powerful wealth creation opportunity. The combination of strong government support, improving fundamentals, and sector growth is creating a perfect setup.

However, investors should not blindly follow the trend. Real success comes from understanding the business, checking fundamentals, and staying patient. Mid cap PSU stocks offer higher returns but also come with higher risk. Large PSU stocks provide stability but slower growth.

A balanced approach is the best strategy. If you select the right mix and hold for the long term, PSU stocks can become a strong part of your portfolio. The opportunity is real in 2026, but smart decision making will decide your returns.

Related Posts :

![Government Loan Schemes In 2026: Smart Funding Options Every Indian Must Know [With Calculators]](https://governmentcsc.com/wp-content/uploads/2026/03/Government-Loan-Schemes-In-2026-Smart-Funding-Options-Every-Indian-Must-Know-With-Calculators.webp)

Share This Post