Garden Reach Shipbuilders Share Price Target 2026, 2029, 2030, 2040, 2050

Garden Reach Shipbuilders Share Price Target 2026, 2027, 2028

Garden Reach Shipbuilders & Engineers Ltd (GRSE) is a leading defence shipbuilding company in India. The company builds warships like frigates, corvettes, patrol vessels and landing crafts mainly for the Indian Navy and Coast Guard. It also provides ship repair and engineering services. GRSE has a strong legacy since 1884 and is one of the key players in India’s defence manufacturing ecosystem.

In the last few years, the company has shown strong financial growth. Revenue increased from around ₹1,100 crore in FY20 to ₹2,700 crore in FY24. Net profit also grew from around ₹120 crore to ₹360 crore.

This shows strong execution and increasing order inflow. Promoter holding is above 70 percent which reflects strong government backing. The company also maintains low debt which reduces financial risk.

In this blog post we are going to explore the Share Price Target of the Garden Reach Shipbuilders from 2025-2050 with the help of fundamental & numeric data & see how much returns can you expect from this share. So keep reading…

Table of Contents

Garden Reach Shipbuilders Share Price Target 2026

| Year | Month | Share Price Target |

|---|---|---|

| 2026 | Jan | ₹2000 |

| 2026 | Dec | ₹4600 |

The company is expected to receive more defence contracts from the Indian Navy. Government focus on domestic shipbuilding is increasing which directly benefits GRSE. Export opportunities are also opening up. Many countries are looking for cost effective defence ships. GRSE can capture this demand.

The strong order book gives revenue visibility for next few years.

Garden Reach Shipbuilders Share Price Target 2027

| Year | Month | Share Price Target |

|---|---|---|

| 2027 | Jan | ₹9500 |

| 2027 | Dec | ₹15500 |

By 2027, GRSE can benefit from both defence and commercial shipbuilding. The company is investing in modern shipbuilding technologies. It is also improving production efficiency which helps in better margins. International expansion can become a major growth driver in this phase.

Garden Reach Shipbuilders Share Price Target 2028

| Month | Share Price Target |

|---|---|

| January | ₹14500 |

| December | ₹20500 |

Global demand for defence ships is increasing. GRSE has a strong position in this market. The company is also focusing on energy efficient ships and new designs. This will help in getting more orders from both domestic and international clients.

Garden Reach Shipbuilders Share Price Target 2029

| Year | Jan Target | Dec Target |

|---|---|---|

| 2029 | ₹19500 | ₹26000 |

GRSE is improving its supply chain and production capabilities. This will help in faster execution of projects. More contracts from defence sector will support revenue growth. The company’s strong reputation also helps in winning repeat orders.

Garden Reach Shipbuilders Share Price Target 2030

| Month | Share Price Target |

|---|---|

| January | ₹25500 |

| December | ₹31000 |

By 2030, GRSE may become a major global shipbuilder. The company is investing in new technologies and modernization. Strong government relationships and stable financials will support long term growth.

Garden Reach Shipbuilders Share Price Target 2040

| Year | Jan Target | Dec Target |

|---|---|---|

| 2040 | ₹58500 | ₹63700 |

In long term, GRSE can expand globally and secure large contracts. The company’s focus on innovation and sustainability will keep it competitive. India’s defence budget growth will continue to support the company.

Garden Reach Shipbuilders Share Price Target 2050

| Year | Month | Share Price Target |

|---|---|---|

| 2050 | Jan | ₹93500 |

| 2050 | Dec | ₹99000 |

In very long term, GRSE can remain a strong defence player. The company has strong entry barriers in shipbuilding. With continuous demand for defence ships, long term growth looks strong.

Should I Buy Garden Reach Shipbuilders Share?

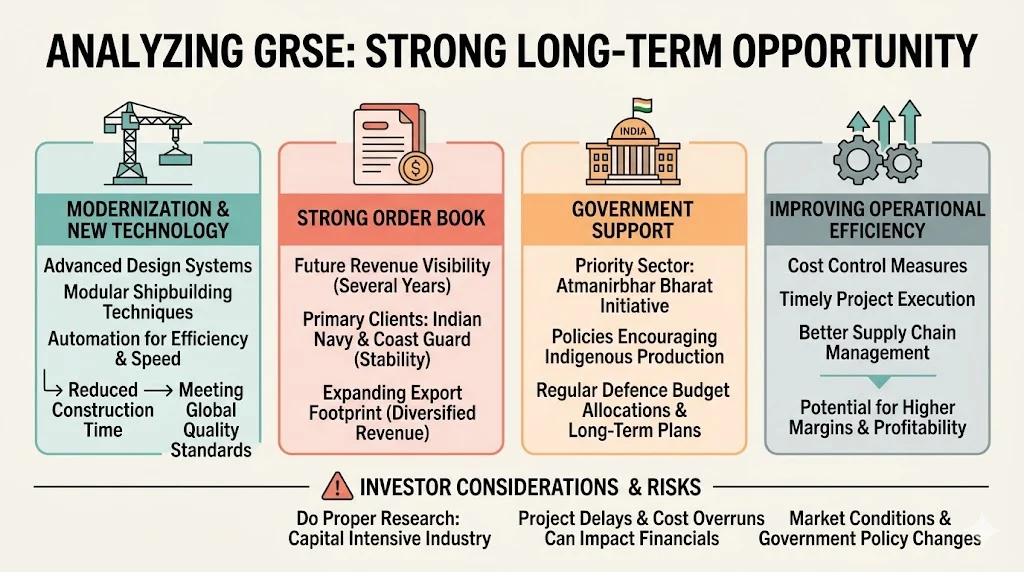

GRSE is focusing on modernization and new shipbuilding technologies. The company is investing in advanced design systems, modular shipbuilding techniques, and automation to improve efficiency and reduce construction time.

These upgrades not only enhance productivity but also help GRSE meet global quality standards, making it more competitive in both domestic and international markets.

The company has a strong order book which ensures future revenue visibility for several years. A large portion of these orders comes from the Indian Navy and Coast Guard, which provides stability and reduces uncertainty in earnings. Additionally, GRSE is gradually expanding its export footprint by securing contracts from friendly foreign nations, which can further diversify its revenue streams.

Government support is also strong as defence manufacturing is a priority sector under initiatives like Atmanirbhar Bharat. Policies encouraging indigenous production and reduced dependence on imports directly benefit companies like GRSE. Regular defence budget allocations and long-term procurement plans provide a steady pipeline of opportunities for the company.

Another positive factor is GRSE’s improving operational efficiency. The company is focusing on cost control, timely project execution, and better supply chain management. These improvements can lead to higher margins and better profitability over time.

However, investors should always do proper research before investing. The shipbuilding industry is capital intensive and project-based, which means delays in execution or cost overruns can impact financial performance. Market conditions, government policy changes, and global economic factors can also influence stock prices.

Overall, GRSE presents a strong long-term opportunity due to its strategic importance, solid order book, and government backing. But like any stock, it carries risks, and investors should evaluate their risk tolerance and investment horizon before making decisions.

Is Garden Reach Shipbuilders Stock Good to Buy (Bull Case & Bear Case)

Bull Case:

- Strong order book ensures future revenue

- Government support for defence sector

- Low debt company

- Growing export opportunities

- Improving margins and efficiency

The bull case for Garden Reach Shipbuilders looks strong due to multiple structural advantages. The company has a healthy and visible order book which provides revenue certainty for the next few years. This reduces business risk and gives investors confidence in future earnings growth. Government support is another major factor, as India is actively promoting domestic defence manufacturing under initiatives like Atmanirbhar Bharat. This ensures a steady flow of contracts for companies like GRSE.

Additionally, the company operates with very low debt, which improves financial stability and reduces interest burden. This allows more profits to be retained and reinvested into business expansion. Export opportunities are also increasing as many developing countries are looking for affordable defence ships. GRSE has already started tapping into this segment, which can significantly boost revenue in the long term.

Improving margins and operational efficiency further strengthen the bull case. With better project execution and cost control, the company can enhance profitability over time.

Bear Case:

- High dependence on government contracts

- Project delays can impact revenue

- Competition from other shipbuilders

- Cyclical nature of shipbuilding industry

Despite strong positives, there are certain risks investors should consider. The company is highly dependent on government contracts, especially from the Indian Navy and Coast Guard. Any delay in defence spending or policy changes can directly impact order inflow.

Project delays are another key concern in shipbuilding. Since these are large and complex projects, even small delays can affect revenue recognition and profitability. Competition is also increasing from other public and private shipbuilders, which may impact future order wins.

Lastly, the shipbuilding industry is cyclical in nature. Demand can fluctuate based on economic conditions and defence budgets. This can lead to periods of slower growth, making the stock volatile in the short term.

Quantitative Analysis of Garden Reach Shipbuilders

| Metric | Value | Analysis |

|---|---|---|

| Revenue Growth | Strong (20%+) | Consistent growth in business |

| Profit Growth | Strong | Healthy earnings expansion |

| EPS Trend | Rising | Indicates better profitability |

| ROE | ~22% | Good return ratio |

| Debt-to-Equity | Low (~0.05) | Financially stable |

| Net Profit Margin | ~13% | Stable margins |

| Market Cap | ₹23K+ Cr | Mid-large cap |

| Dividend Yield | ~0.6% | Stable income |

| Promoter Holding | ~73% | Strong government backing |

Revenue growth is strong and consistent, which clearly reflects the rising demand for defence shipbuilding and engineering services. Over the past few years, GRSE has benefited from a steady inflow of orders from the Indian Navy and Coast Guard, along with increasing export opportunities. This consistent revenue expansion indicates that the company is successfully executing its projects and maintaining a strong pipeline of future contracts. The growth is not just volume-driven but also supported by improved project execution timelines and better cost management, which enhances overall operational efficiency.

Profit growth is also healthy and in many cases growing faster than revenue, which highlights the company’s improving operational leverage. This means GRSE is able to control its costs effectively while increasing output, leading to higher profitability. The company has been focusing on optimizing its production processes, reducing delays, and improving supply chain efficiency. As a result, profit margins have remained stable and even shown gradual improvement over time. This strong profit growth reflects the company’s ability to convert revenue into actual earnings, which is a key indicator of financial strength.

Return on Equity (ROE) around 22 percent is considered very strong, especially for a PSU company. This indicates that GRSE is efficiently utilizing shareholder capital to generate profits. A high ROE suggests that the company is not only profitable but also disciplined in its capital allocation.

It shows that management is effectively reinvesting earnings into projects that generate good returns. For long-term investors, a consistently high ROE is a positive signal as it reflects sustainable business performance and efficient management practices.

Debt levels in the company are very low, which significantly reduces financial risk. GRSE operates with a near debt-free balance sheet, which means it does not have a heavy burden of interest payments. This gives the company greater financial flexibility to invest in new projects, upgrade technology, and expand its capabilities without worrying about repayment pressure. In uncertain economic conditions, companies with low debt are generally more stable and resilient. This strong balance sheet position also enhances investor confidence and supports long-term growth.

Margins are stable, which indicates consistent performance across different business cycles. Despite fluctuations in raw material costs and project timelines, GRSE has managed to maintain steady profit margins. This stability is a result of efficient cost control, better project management, and a favorable product mix. Stable margins also suggest that the company has pricing power and can manage cost pressures effectively. Over time, as the company moves towards more advanced and high-value shipbuilding projects, there is potential for further margin expansion.

Promoter holding is high, at around 73 percent, which provides strong stability to the stock. Since the Government of India is the majority shareholder, it ensures long-term strategic support and policy backing. High promoter holding also reduces the risk of sudden large-scale selling in the market, which can create volatility. It reflects confidence from the promoters in the company’s future growth prospects. Additionally, government backing ensures a steady flow of defence contracts, which strengthens revenue visibility and business continuity.

Overall, the quantitative metrics of GRSE highlight a financially strong and well-managed company. The combination of consistent revenue growth, strong profitability, high ROE, low debt, stable margins, and strong promoter backing makes it an attractive long-term investment opportunity in the defence sector.

Conclusion

Garden Reach Shipbuilders is a strong defence company in India. The company has shown steady growth in revenue and profit.

Its strong order book and government support give good future visibility. The company is also improving its technology and expanding globally. Overall, GRSE looks like a strong long term stock in defence sector.

If you are someone who believes in India’s defence growth story, this stock can be worth keeping on your radar. But don’t rush into it just because of the hype. Take your time, understand the business, and see if it fits your investment goals. Markets can be unpredictable, so it’s always better to stay patient and invest with a clear plan. In the end, smart investing is not about chasing returns, but about making informed and confident decisions.

Related Posts :

![Government Loan Schemes In 2026: Smart Funding Options Every Indian Must Know [With Calculators]](https://governmentcsc.com/wp-content/uploads/2026/03/Government-Loan-Schemes-In-2026-Smart-Funding-Options-Every-Indian-Must-Know-With-Calculators.webp)

Share This Post